True value goes far beyond just financial metrics or expanding profit margins, rather, it is about recognizing the success of a business is deeply intertwined with the well-being of key stakeholders (customers, investors, and employees) and that sustainable and resilient growth and profitability arise from a balanced approach to value creation.

In this white paper we will focus on a framework you can use to unlock the true value of your company. This involves shifting from zero-sum strategies to a win/win philosophy, where investments in innovation, employee development, and customer satisfaction drive long-term growth and stability. By taking the time to develop a well-thought-out roadmap that includes broadening organizational goals, focusing on sustainable value creation, and embracing pragmatic idealism, companies can unlock their true value potential and secure a competitive advantage that will last in good times and bad.

Defining True Value Potential

Achieving a company's true value goes beyond financial metrics; it involves creating sustainable value for customers, employees, and investors. This holistic approach acknowledges that the interests of these three groups are interconnected, and that true value is only created when it benefits all stakeholders.

For customers, it means offering products and services that meet their needs with innovation and precision. For employees, it involves respect, involvement in decision-making, meaningful work, excellent compensation opportunities, and continuous development. And for investors, it translates into delivering consistently high returns on their capital, fostered by strong revenue growth and profit margins that result from sustained value delivery to customers and employees alike.

The Importance of Achieving True Value in Today’s Economy

If the past few years has taught us anything, it's that businesses must be ready for the unexpected. From a global pandemic to the most aggressive interest rate hiking campaign seen in the last 40 years, businesses have faced an unprecedented number of challenges.

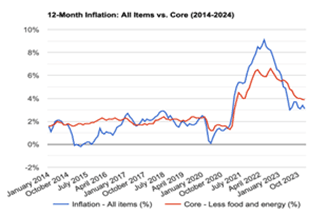

The latest CPI print showed inflation is proving to be stickier than most expected (see chart above) and interest rate cuts are now expected to be delayed longer than most economists and investors thought. This reality translates into broader economic uncertainty as central banks keep a restrictive stance to bring inflation back down to 2%. And although economic growth has shown surprising resilience, there is an elevated risk that the economy could begin to contract in the coming quarters.

In volatile environments, the pursuit of true value becomes not just an advantage but a necessity for survival and growth. Great companies are built off difficult times, and right now is a great time for business owners to prove they have a business model that can provide value to customers at all times.

Roadmap to Unlocking True Value Potential

This begins with redefining the organization's mission around its value-adding activities – be it as a provider of quality products, exceptional services, or innovative solutions.

Here's a structured roadmap for businesses aiming to achieve this:

- Redefine Organizational Self-Interest: Broaden the goals beyond short-term financial metrics to include the well-being of customers, employees, and the larger community. This shift encourages investments in areas like R&D, employee development, and customer engagement that are critical for long-term value creation.

- Expand the Pie: Adopt strategies that do not merely redistribute existing value but create additional value. For example, flexible work schedules, investment in employee training, and partnerships that align the interests of the company with those of its employees and customers can lead to enhanced productivity, improved customer satisfaction, and ultimately, higher returns for investors.

- Balance Sheet Dynamics for Strategic Assets: Identify and manage the key assets that drive value creation – customer loyalty, employee engagement, process efficiency, and investor confidence. Develop metrics and reporting systems that reflect the growth and health of these intangible assets alongside traditional financial metrics.

- Be Optimistic & Realistic: Navigate business decisions with a strong level of optimism, though remain realistic in what can be accomplished in a given time frame. Be ready to pivot, accept that mistakes will be made along the way, and remain focused on the end goal of true value creation.

- Innovate and Adapt: Innovation and embracing change will be a key factor throughout this entire process. Businesses that are ready to embrace a culture that focuses on product development, service delivery, and improved business processes will set themselves up for success in the long term.

Understand Your Company's True Value Potential

We start with assessing your current performance and pinpointing growth opportunities.

Assess Current Business Performance and Identify Growth Opportunities

Achieving steady, predictable growth is a hallmark of successful companies, yet only a small percentage manage to attain this level of performance consistently. This underscores the need to rigorously assess current business performance, not only in financial terms but also in operational effectiveness, market positioning, and strategic agility. Identifying growth opportunities requires a keen understanding of market dynamics, customer behaviors, and new technology.

Outline Key Success Factors

Outliers in achieving steady growth share common traits that transcend industry specifics or geographic location. These include:

- A commitment to continuous innovation, an options-oriented approach to market entry, and a knack for making strategic buys.

- Managing major resource allocations centrally and fostering a culture that supports speed, flexibility, and innovation.

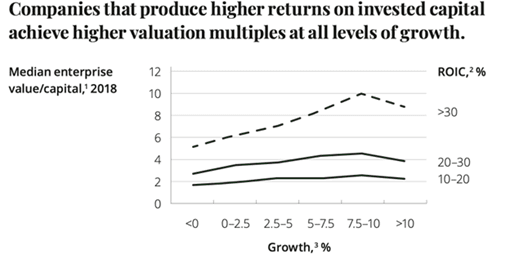

Strategically investing capital into assets that generate meaningful revenue growth – High ROIC (Return on Invested Capital) – have a higher chance of finding success in expansion initiatives compared to firms who show lower ROIC (see chart below).

Identify Competitive Advantages

Competitive advantages stem not from a company's size, age, or market but from its ability to adapt and innovate while maintaining a stable core of leadership, strategy, and values. Identifying competitive advantages require a deep dive into what makes the company unique – be it approach to innovation, price point, corporate culture, or ability to rapidly adjust to market changes while keeping strategic priorities intact.

Analyze Market Trends

Leveraging market intelligence to help make strategic decisions, moving early into attractive markets, and diversifying portfolios to manage risks are key parts of success. This applies to both current states as well as anticipating future developments using a combination of data analysis and customer insights to guide strategic direction.

Understand the Customer’s Needs to Fuel Expansion Strategies

Knowing the customers’ needs goes beyond responding to current demands; it's also about anticipating future needs and innovating accordingly. By predicting and addressing what customers will require before they may realize it themselves, companies can stay ahead of the curve.

Creating Your Strategic Approach

A proper strategic approach involves setting clear and achievable goals, understanding the market, and meticulously planning expansion strategies while being acutely aware of potential risks and regulatory hurdles.

- Set Clear and Achievable Business Goals and Objectives (KPIs)

The starting point of any new expansion plan, project, or strategy, to unlock value is deciding what will be measured and how. Key Performance Indicators (KPIs) need to include both short-term goals and long-term ambitions.

- Incorporate KPIs into Your Growth Strategy

KPIs should reflect the company’s mission, the well-being of its stakeholders, and its commitment to contributing positively to society. This ensures that growth is not just profitable but also sustainable, resilient, and aligned with the broader objectives of management.

- Identify Current Consumers and New Consumer Segments for Expansion

Successful expansion is about ensuring that core consumers remain engaged and satisfied, while simultaneously exploring new areas that promise growth and diversification. This exploration is guided by data, trends, and insights that reveal where the market is headed, what new needs are emerging, and how consumer behaviors are shifting.

Develop Expansion Strategy

To achieve sustainable growth explore a variety of expansion strategies tailored to the market, capabilities, and growth objectives. Each strategy offers a unique path to increase share, enter new markets, or diversify product lines. Key expansion strategies:

Market Penetration

Focus on increasing the market share of an existing product in its current market through aggressive marketing and sales tactics. This can involve:

- Enhanced Marketing Efforts: Increasing advertising, promotions, and sales activities to boost product visibility and attract more customers from the existing market.

- Competitive Pricing Strategies: Adjusting pricing to make the product more appealing compared to competitors, potentially attracting a larger customer base.

- Customer Loyalty Programs: Creating incentive programs to retain existing customers and increase the frequency of their purchases.

Product Development

Introduce new products or improve existing products to meet evolving customer needs. This can include:

- Innovation: Developing new products that offer unique benefits or solve existing problems more effectively than competitors.

- Product Enhancement: Upgrading current products to enhance their appeal or introduce new features that meet additional customer needs.

- Technology Integration: Incorporating the latest technologies into products to improve functionality, efficiency, or user experience.

Market Development

Aimed at entering new markets or segments with existing or slightly modified products. This can include:

- Geographic Expansion: Extending the product’s reach into new geographical areas, both domestically and internationally.

- Targeting New Segments: Identifying and targeting new customer segments within existing markets or in new markets, which may have different needs or preferences.

Diversification

Expand into new markets with new products, significantly reducing dependency on current markets or products. This strategy usually includes:

- Related Diversification: Entering new but related markets or product areas where the company can leverage its existing strengths or competencies.

- Unrelated Diversification: Venturing into entirely new lines of business, offering new products or services that are not related to the existing portfolio, to spread risk and explore new growth opportunities.

Identify Potential Risks and Overcome Them

Identifying risks is not just about spotting hazards, it's about crafting a solid plan to navigate through them. This involves assessing both the internal and external conditions for things that could throw a company off course, including market volatility, regulatory changes, and technological disruptions.

Developing a risk management strategy is about more than having a backup plan, it involves integrating risk anticipation into your expansion planning, ensuring that your business can withstand and adapt to changes in the economic and competitive environment. This may include diversifying your supply chain, building new partnerships, or investing in technology that can give you a competitive edge in times of change.

Consider Regulatory and Compliance Issues

Beyond focusing solely on environmental, social, and governance (ESG) initiatives, companies should consider a wider spectrum of regulatory restrictions and compliance requirements across different markets and industries. This will ensure not only adherence to legal standards but also foster trust among stakeholders, thereby enhancing the company's reputation and contributing to its sustainable growth.

When planning for expansion, conduct thorough due diligence to understand the specific regulatory frameworks of new markets, including local laws, industry regulations, and international standards that might apply. This involves assessing everything from data protection and privacy laws to labor standards and anti-corruption measures.

Internally, develop robust compliance programs that are adaptable to the nuances of different regulatory environments. These programs should include clear policies, employee training, regular audits, and mechanisms for reporting and addressing compliance issues.

Assess and Allocate Resources and Budget for Expansion

There is no set or correct way to manage funds and budgets, rather, the importance should be on ensuring your most important projects are well-funded and the right people are working on them. With any large project, compromises will have to be made and budgetary constraints will force decision makers to choose between different options. Remaining flexible is the most important takeaway when managing a budget, as well as being ready to pivot, adjust, or cut funding to projects that underperform.

Employ the Best Tactics for Successful Business Expansion

From setting clear goals, identifying risks, and allocating resources, the above framework provides a strong outline of where business owners should put their time when preparing to expand and unlock their business’s true value.

Now, we turn our attention to the execution and the specific areas of the business on which we need to focus.

Marketing Strategies: Define the Right Entry Mode for Your Business

Selecting the optimal market entry strategy will be one of the first things to do when looking to expand into new territories or industries. Each approach varies in complexity, risk, and investment requirement, making the decision highly contingent on a company’s specific goals, available resources, and the nuances of the target market.

Below breaks down different entry strategies to consider:

- Licensing: This involves a company (the licensor) granting rights to another company (the licensee) to produce and sell its products or use its technology in exchange for a royalty fee. Licensing can be a low-risk, cost-effective way to enter foreign markets, leveraging the licensee's existing manufacturing, distribution networks, and local market knowledge.

- Franchising: Similar to licensing, franchising allows a business to operate using the franchisor's brand, products, and operational model in return for a fee and ongoing royalties. This model is commonly used in the retail, restaurant, and service sectors. It provides a way to expand rapidly with relatively lower capital investment and risk.

- Joint Ventures: Involves partnering with a firm to create a new entity, shared by both companies. This approach allows for shared risk, resources, and market knowledge, facilitating easier access to new markets. It requires significant investment and collaboration but offers more control compared to licensing or franchising.

- Acquisitions: Buying an existing company in the target market is a fast entry strategy that provides immediate market access, an established customer base, and operational capabilities. While it involves significant upfront investment and potential integration challenges, acquisitions offer complete control over operations and strategic direction in the new market.

- Direct Exporting: Selling directly to customers in a new market is the simplest form of expansion but can be challenging due to the need for extensive market research, distribution logistics, and potential tariff barriers. Companies may use their sales team or hire agents/distributors to manage sales in the target market.

- Greenfield Investments: Involves starting a new venture from scratch in the target market, offering complete operational control and the ability to build the business to exact specifications. However, it represents the highest risk and investment, requiring significant time and resources for market research, site selection, construction, and recruitment.

Market Research: Conduct Feasibility Studies for Strategy Implementation

Understanding the target market's pain points via market research aids in tailoring products or services to meet specific needs but also in differentiating your business from competitors. Market research provides the data necessary to craft a unique selling proposition (USP) that resonates with the new market segments.

The following is a step-by-step guide:

- Define Your Objectives. Clearly outline what you hope to learn from your market research from understanding customer preferences to identifying potential market segments.

- Choose Your Research Method. Decide between primary research (conducting surveys, interviews, or focus groups directly with potential customers) and secondary research (analyzing existing data from reports, studies, and other sources).

- Segment Your Market. Break the market into segments based on demographics, behaviors, or needs to tailor your approach and identify the most promising segments for expansion.

- Collect Data. Use the chosen research method to gather information (e.g., deploying surveys, conducting interviews, or analyzing industry reports).

- Analyze the Data. Look for patterns, trends, and insights within the data collected.

- Develop Your Unique Selling Proposition (USP). Based on the insights gathered, craft a USP that addresses the identified needs and sets your offering apart from competitors.

- Test Your Findings. Validate research findings and USP with a smaller, targeted group from the intended market to ensure it resonates before a full-scale launch.

- Refine Based on Feedback. Use feedback from the testing phase to refine the product, service, or marketing strategy.

Branding: Evolve Branding Elements to Support the Strategy

Adapt your brand message, visuals, and overall communication strategy to appeal to new customer segments while retaining your brand's core identity. Effective brand evolution supports market entry and expansion efforts by fostering brand recognition and trust.

Marketing: Implement Campaigns and Promotions to Create Awareness

Implement targeted marketing campaigns and promotions to create awareness in new markets by leveraging both digital and traditional marketing channels to reach potential customers effectively. Tailored campaigns that address the specific pain points and needs of the new market will significantly enhance market penetration and brand visibility.

Sales and Distribution: Adapt Sales and Distribution Strategies

Adapt the sales and distribution strategies to fit new market dynamics via a thorough analysis of the new market's unique characteristics and consumer behaviors to develop a tailored approach that maximizes reach and efficiency. Here's a closer look at the components of adapting sales and distribution strategies:

- Establish New Distribution Channels. Investigate and utilize channels that match local buying habits (e.g., online marketplaces or partnerships with local entities).

- Partner with Local Distributors. Leverage market knowledge and networks to penetrate the market more effectively and navigate local regulations/cultural nuances.

- Leverage E-commerce Platforms. Use online platforms to access customers across different regions and adapt strategies to fit popular e-commerce habits in the new market.

- Implement Flexible Pricing Strategies. Adjust pricing to reflect the new market's economic conditions and maintain competitiveness without sacrificing profitability.

- Customize Marketing and Sales Materials. Ensure materials are culturally relevant and in the local language to better connect with the target audience.

- Train Sales Teams. Equip teams with knowledge on local market dynamics and cultural practices to enhance their effectiveness.

- Adapt Based on Feedback. Be ready to adjust strategies based on market response and customer feedback to ensure success.

Your sales and distribution plan will be founded on the market research done earlier, which will help narrow the focus to be on the most effective and lowest cost way to effectively distribute your product or service.

Training: Align Employees with the New Strategic Approach

All expansion plans require a well-trained staff that is ready to deal with the complexities and new challenges that will arise with moving into a new market. By investing in comprehensive training programs, companies not only empower their employees but also enhance their ability to innovate and respond to market challenges. This proactive approach to workforce development ensures a team will not only be prepared for the immediate tasks at hand but will also equip them to drive long-term growth and contribute to the successful move into new markets.

Operations: Adapt Processes and Infrastructure

This step is a critical move that, if mishandled, can lead to significant financial setbacks. To navigate this transition effectively and avoid unnecessary expenses, businesses should consider a simplified three-step approach:

Strategic Alignment and Incremental Implementation

- Strategic Alignment. Begin by ensuring that any changes to operations or infrastructure are in direct alignment with the broader strategic goals of your business to ensure investments are focused and contribute to long-term growth (rather than short-term fixes).

- Incremental Implementation. Adopt a phased approach to integrating new technologies or processes by implementing changes in stages to assess their impact, adjust as necessary, and manage costs more effectively.

Invest in Training and Scalable Solutions

- Workforce Training. Equip teams with the knowledge and skills needed to adapt to new operational procedures or technologies.

- Scalable Solutions. Choose technologies and infrastructure options that can grow with the company. Scalable solutions help avoid the need for costly overhauls as your business expands, ensuring a smoother scaling process.

Ongoing Evaluation and Regulatory Compliance

- Continuous Evaluation. Regularly assess the effectiveness of operational changes against set benchmarks and KPIs to identify areas for improvement and ensure that the operational strategy remains cost-effective.

Talent: Upskill or Recruit to Support Growth

The upskilling of your workforce needs to be in line with the training plan, as well as planned changes to operations. A common mistake is to overlook the integration of training efforts with the broader strategic changes, leading to a misalignment between employee capabilities and the company's evolving needs. To avoid this, ensure upskilling initiatives are directly linked to the new strategic directions and operational methodologies your business is adopting.

Establish Benchmarks and Targets for Monitoring Progress

Take the KPIs and decide upon the benchmarks or realistic targets that will align with strategic goals and objectives. Establishing benchmarks requires a deep understanding of industry standards, competitor performance, and historical data within your organization. It's about striking a balance between what's aspirational and what's achievable, ensuring that targets push the company forward without setting it up for failure.

Risks/Challenges: Have Contingency Plans in Place

Having long and detailed contingency plans can be a waste of time, instead take the time to create smaller game plans. This agile methodology allows for quicker responses to unforeseen challenges, ensuring that the business can adapt and pivot without losing momentum. Each smaller plan should outline potential risks, triggers for action, and steps to mitigate the impact, keeping the broader strategic goals in sight.

Furthermore, foster a culture that embraces change and encourages flexibility among teams. Empower employees to make decisions and take actions that align with contingency plans and the company's strategic objectives. Regular training and simulations on handling unexpected situations can enhance this adaptability, making your team more resilient and prepared.

Conclusion

To realize a company's true value potential it's crucial to revisit the key insights and strategies that we covered that drive true value, sustainable growth, and success.

- Achieving True Value. Unlocking the true value of a company will require business owners to take the perspective of the customer, employee, and investor. Only when all three are benefitting will the true value of a company develop.

- Strategic Approach to Expansion. Creating a strategic blueprint entails setting achievable business goals, identifying growth opportunities, assessing risks, ensuring regulatory compliance, and dynamically allocating resources to support your expansion initiatives.

- Employing Successful Tactics. The path to successful business expansion is paved with carefully crafted marketing strategies, thorough market research, adaptive branding, targeted promotions, and an agile approach to sales, distribution, operations, and talent management – underscored by the importance of monitoring progress through established benchmarks.

As businesses today deal with more uncertainty than ever before, companies need to proactively pursue growth, expansion, and the discovery of their true value if they want to secure their future. By adopting a proactive stance, businesses can not only seize emerging opportunities and maintain a competitive edge but also adapt swiftly to changing market conditions, consumer preferences, and economic uncertainties.

For more information on how MatrixPoint can help unlock your business’ true value potential contact Benson Hausman at Bhausman@thematrixpoint.com.